The Bonus as Financial Instrument: Why Your “Target” Was Never Meant to Be Paid

The Pattern Everyone Recognizes But Few Examine

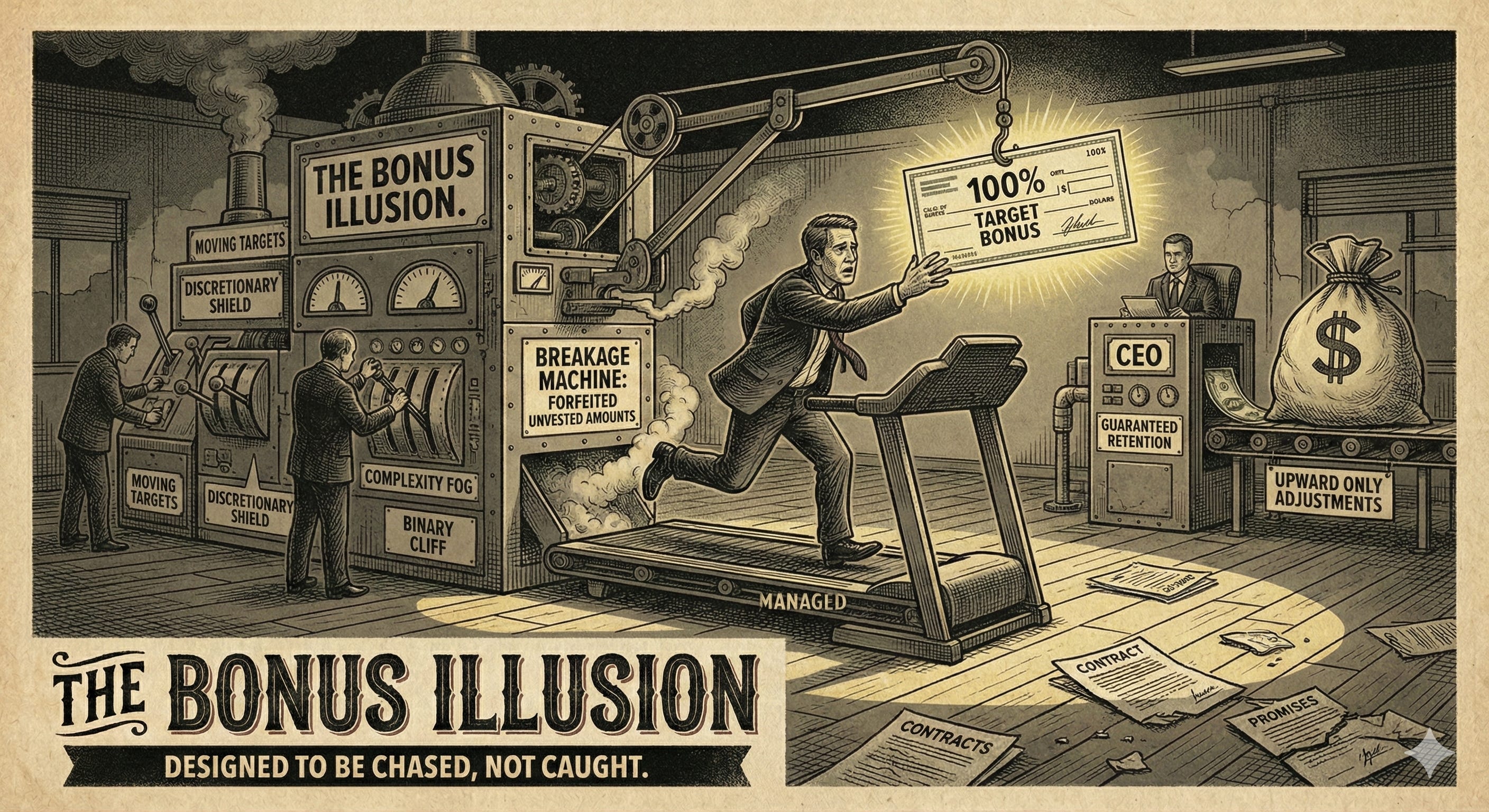

Every fiscal year, the ritual repeats with predictable precision. Employees meet or exceed their performance targets. Managers deliver positive reviews, occasionally glowing ones. The organization’s financial results appear solid, sometimes exceptional. And then, with carefully constructed regret, the bonus arrives diminished—not eliminated entirely, no…